Loan Deferment: Hitting Pause, Not Stop, on Your Financial Journey

Ever feel like life handed you a financial curveball right when you were starting to get your stride? Maybe you just graduated with student loans looming larger than your career prospects, or perhaps an unexpected medical bill knocked your budget off balance. That’s when loan deferment can feel like a lifesaver—kind of like hitting the snooze button on your debt, only without the guilt (well, maybe a little).

Let’s be real: money can get messy, and nobody’s got it all figured out. But having the option to pause your loan payments when times are tough? That’s a game changer.

What Exactly Is Loan Deferment?

Loan deferment means your lender lets you temporarily stop making payments on your loan.

Simple, right? Kinda. The twist is interest may still accrue depending on what kind of loan you’ve got.

Usually, people apply for deferment when they’re:

-

In school

-

Unemployed

-

Facing financial hardship

-

On military duty

Think of it as a financial breather—like pressing “pause” on Netflix when life gets too chaotic to focus on the story.

My “Oops, I Need a Break” Moment

A few years ago, I was juggling student loans, a car payment, and rent while trying to get a freelance career off the ground. Then—boom—my biggest client ghosted me. You know that sinking feeling when you open your banking app and it looks like a desert? That was me.

That’s when a friend (seriously, bless her) mentioned loan deferment. After a few calls and some paperwork, my lender approved it, giving me six months of breathing room. Those months were pure gold—I got back on my feet, found new clients, and avoided defaulting altogether.

That experience taught me something huge: deferment isn’t failure; it’s strategy.

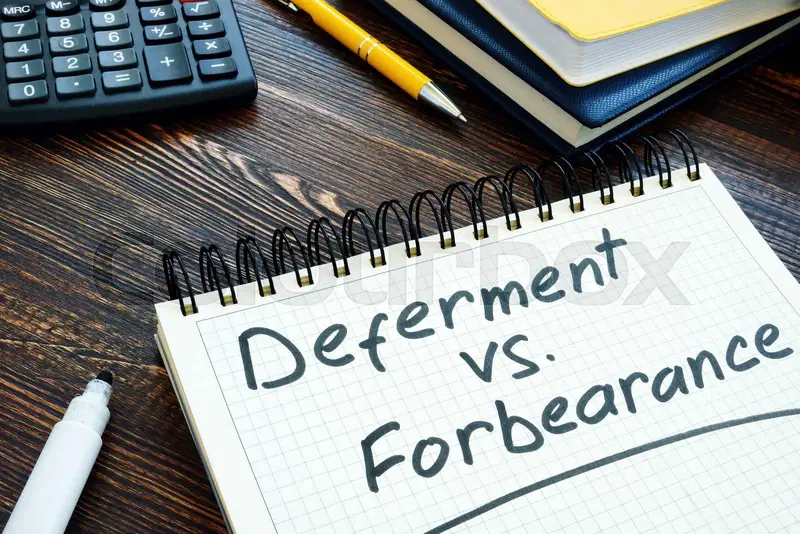

Deferment vs. Forbearance: What’s the Difference?

Ah, the age-old confusion. People toss these terms around like they’re identical twins—but they’re more like cousins.

| Feature | Loan Deferment | Loan Forbearance |

|---|---|---|

| Purpose | Temporary pause due to specific qualifying reasons (school, unemployment) | Pause or reduce payments due to hardship |

| Interest Accrual | Depends on loan type (some may not accrue) | Always accrues interest |

| Duration | Usually longer (up to 3 years) | Shorter (12 months at a time) |

| Eligibility | Must meet lender’s qualifying criteria | More flexible but costlier long-term |

So basically, deferment’s the cheaper pause; forbearance’s the “well, it’s better than default” option.

How to Qualify for Loan Deferment

Getting approved isn’t as tricky as it sounds, but it does require a few steps:

-

Contact your lender early – Do not wait until payments are past due.

-

Explain your situation – Whether it’s unemployment, returning to school, or financial hardship, clarity helps.

-

Submit paperwork – Yep, there’s always paperwork.

-

Stay in communication – Follow up to confirm approval.

Pro tip: lenders love proactive borrowers. Being upfront shows responsibility—and that can even boost your credit trustworthiness over time.

The Good, the Not-So-Good, and the Gotta-Know

Like every financial decision, deferment has pros and cons.

The Good

-

Breathing space to regain control of your finances.

-

Avoiding late fees or loan default damage to credit.

-

Keeping federal protections (for student loans).

The Not-So-Good

-

Interest may pile up quietly in the background.

-

You’re delaying progress on paying down principal.

-

Some private lenders charge reinstatement fees afterward.

The Gotta-Know

Use your deferment time smartly—budget, build savings, maybe even pick up a side hustle. Treat it as a temporary pit stop, not a vacation.

Student Loan Deferment: The Most Common Case

For many, this is where deferment becomes a real lifeline.

Federal student loan borrowers have multiple deferment options:

-

In-School Deferment: As long as you’re enrolled half-time, payments pause automatically.

-

Unemployment Deferment: If you’re actively seeking work.

-

Economic Hardship Deferment: For genuine financial struggles.

-

Military Deferment: While serving active duty.

By the way, if you’ve got subsidized loans, the government may even cover the interest during deferment. Pretty sweet, huh?

Private Loan Deferment: A Whole Different Beast

Private lenders? They play by their own rules. Some offer deferment in special cases; others don’t at all. Always read the fine print and negotiate politely but persistently.

My advice? Call your lender before skipping a payment. You’d be surprised how flexible they can be when you’re transparent.

Should You Choose Deferment or Just Tough It Out?

That depends on your situation.

If you’re in a short-term pinch—like switching jobs or dealing with unexpected bills—deferment’s perfect.

But if you can at least make interest payments? It’s worth it. Keeps the loan balance from ballooning and helps your credit score.

As my dad used to say, “Just because you can hit pause doesn’t mean you should forget the song.”

Expert Insights: When Deferment Makes the Most Sense

Financial advisors typically recommend deferment when:

-

You expect your income to bounce back soon.

-

You’re investing in education that’ll boost future earning power.

-

You’re avoiding high-interest alternatives like credit cards.

However, if your income drop looks long-term, consider income-driven repayment plans instead.

Common Loan Deferment Myths (Busted!)

-

Myth #1: It ruins your credit.

Nope! As long as payments were current before approval, deferment doesn’t harm credit. -

Myth #2: You can defer endlessly.

Sorry, that’s fantasy. Lenders cap how long you can pause payments—usually up to 36 months. -

Myth #3: It’s automatic.

Absolutely not. You must apply and get approved.

FAQs About Loan Deferment

1. Does interest accrue during deferment?

Yes, for unsubsidized and private loans. Subsidized loans may pause interest.

2. Can deferring help credit score?

Indirectly. It prevents missed payments, which protects your score.

3. How long can I defer payments?

It depends on loan type—some allow up to three years per deferment period.

4. What are alternatives if I don’t qualify?

Forbearance or income-driven repayment plans are solid alternatives.

Final Thoughts: Deferment Is a Tool, Not a Crutch

Deferment isn’t a sign of defeat—it’s financial flexibility. It buys you time to stabilize and plan smarter moves.

But don’t treat it like a magic fix. When possible, keep making small payments. Future You will thank Present You.

And hey, if you’re on the fence about applying? Talk to your lender, a financial advisor, or even someone who’s been there. Real stories, real advice—that’s where the gold is.